Pre-ECB Monetary Systems and the Bank of Amsterdam Legacy (1700, 1900)

The Bank of Amsterdam (Amsterdamsche Wisselbank), operational from 1609 to 1820, functioned as the world's premier proto-central bank during the 18th century. Unlike modern central banks that manage fiat currency, the Wisselbank operated a ledger-based system backed by precious metals, a structure historians frequently compare to a 100% reserve "stablecoin." Between 1700 and 1760, the Bank maintained a near-perfect ratio of metal reserves to bank money liabilities. This discipline made the bank guilder the de facto reserve currency of Europe. During the liquidity emergency of 1763, the Bank demonstrated early lender-of-last-resort capabilities, expanding its balance sheet by 8 million guilders (approximately 35% of total assets) to inject liquidity into a freezing market. This intervention stabilized the Amsterdam exchange, proving that a central authority could manage widespread risk without debasing the currency.

The Wisselbank's downfall provides the serious lesson in the dangers of fiscal dominance, a lesson enshrined in the ECB's prohibition on monetary financing. Following the outbreak of the Fourth Anglo-Dutch War (1780, 1784), the City of Amsterdam forced the Bank to lend secretly to the Dutch East India Company (VOC). These unsecured loans destroyed the Bank's balance sheet. Data from the Amsterdam Municipal Archives show the reserve ratio plummeted from nearly 100% in 1776 to 20% by 1788. By 1790, the premium (agio) on bank money over coin, and the Bank declared insolvency. The collapse of the guilder as a reserve asset shifted financial hegemony to London, the structural flaw, central bank assets comprised of bad state debt, remained a warning for future European monetary architects.

As the 19th century dawned, two distinct models of central banking diverged in London and Paris, creating a theoretical rift that in modern Eurosystem debates. The Bank of England, following the suspension of convertibility (1797, 1821), adopted a volatile, market-reactive method. Between 1880 and 1914, the Bank of England changed its discount rate frequently to manage gold flows, with a standard deviation of 0. 99. In contrast, the Banque de France, founded in 1800, prioritized stability over market signaling. It maintained a massive gold reserve, reaching nearly 2 billion francs by 1900, dwarfing British reserves, to insulate the domestic economy from external shocks. The Banque de France's discount rate standard deviation was only 0. 57 during the same period. This "French Model" of using a heavy balance sheet to dampen volatility directly influenced the ECB's operational preference for large liquidity buffers over rate volatility.

The mid-19th century saw the attempt at a pan-European currency union: the Latin Monetary Union (LMU), established in 1865 between France, Belgium, Italy, and Switzerland. The LMU was built on a bimetallic standard, fixing the gold-to-silver ratio at 1: 15. 5. This rigid peg proved fatal when silver discoveries in Nevada and the German switch to gold (1873) flooded global markets with silver. The market ratio diverged sharply from the official 1: 15. 5 peg, causing a massive inflow of depreciating silver into LMU mints. By 1878, the union was forced to suspend silver coinage, shifting to a gold standard. The LMU also failed to enforce fiscal discipline among members. Italy suspended convertibility in 1866, barely a year after joining, and printed small-denomination paper money to finance wars, exporting inflation to its partners. The LMU experience demonstrated that a monetary union without a unified fiscal policy or a single central bank to enforce rules was structurally unsound.

| Metric | Bank of England (UK) | Banque de France (France) | Reichsbank (Germany) |

|---|---|---|---|

| Primary Objective | Gold Convertibility / External Balance | Domestic Rate Stability | Gold Standard / Industrial Growth |

| Discount Rate Volatility (SD) | 0. 99 (High) | 0. 57 (Low) | 0. 92 (Medium) |

| Gold Reserves (1900 est.) | ~£30-40 Million | ~£80-90 Million (2B Francs) | ~£40-50 Million |

| Policy method | Rate adjustments | Balance sheet absorption | Bureaucratic credit rationing |

The final pillar of pre-ECB history is the German monetary unification of 1871, 1876. The creation of the Reichsbank in 1876 marked the triumph of the "Prussian" model: a centralized, bureaucratic institution strictly adhering to the gold standard while supporting industrialization. The Reichsbank replaced a chaotic system of 33 separate currencies and multiple notes of problem. It expanded aggressively, growing from 206 branches in 1876 to 330 by 1900, creating a unified payment system that integrated the German economy. The Reichsbank maintained a discount rate consistently higher than the Berlin market rate (by approximately 100 basis points) to attract gold and maintain the currency's external value. This "hard money" tradition, prioritizing currency stability above all else, became the intellectual foundation of the Bundesbank and, subsequently, the primary theoretical template for the ECB.

European Monetary System and Exchange Rate Alignment (1979, 1998)

The following table illustrates the economic that fueled the 1992 breakdown, comparing inflation and interest rate differentials between the anchor economy (Germany) and the peripheral pressures (Italy, UK).

| Year | German Inflation (%) | Italian Inflation (%) | UK Interest Rate (Base) | German Interest Rate (Lombard) |

|---|---|---|---|---|

| 1980 | 5. 4% | 21. 2% | 17. 0% | 9. 0% |

| 1985 | 2. 2% | 9. 2% | 12. 5% | 5. 5% |

| 1990 | 2. 7% | 6. 5% | 14. 8% | 8. 0% |

| 1992 (Sept) | 5. 1% | 5. 2% | 10. 0% (hiked to 15%) | 9. 75% |

In the aftermath of the 1992-1993 turmoil, European leaders did not abandon the project instead loosened the shackles to save it. In August 1993, the fluctuation bands were widened from ±2. 25% to ±15%, creating a "soft" ERM that deterred one-way speculative bets. This period marked the transition from rigid pegs to the convergence criteria laid out in the Maastricht Treaty (1992). The focus shifted to the "Holy Trinity" of convergence: inflation, interest rates, and fiscal deficits. The route to the Euro required brutal fiscal contraction for Southern Europe. Italy, determined to be a founding member of the single currency, executed one of the most dramatic fiscal adjustments in modern history. In 1990, the Italian budget deficit stood at 11. 1% of GDP. By 1997, through a combination of tax hikes (including the "Euro tax") and spending cuts, the deficit was compressed to 2. 7%, meeting the Maastricht limit of 3%. Yet, the debt criterion, 60% of GDP, was blatantly ignored. Italy's debt-to-GDP ratio in 1997 was 122%, European officials accepted a "satisfactory downward trend" as sufficient evidence of compliance, a political compromise that a structural fault line into the Euro's foundation. The institutional to the ECB was the European Monetary Institute (EMI), established in Frankfurt on January 1, 1994. Under the leadership of Alexandre Lamfalussy and later Wim Duisenberg, the EMI did not set monetary policy prepared the regulatory and logistical framework for the single currency. It operated as a shadow central bank, harmonizing statistics and overseeing the preparation of the Euro banknotes. The EMI's existence signaled the end of national monetary sovereignty; by the time the ECB was formally established in 1998, the national central banks had already surrendered their independence in all name, locking their exchange rates irrevocably on December 31, 1998. The era of the Deutsche Mark, the Franc, and the Lira had ended, replaced by a supranational experiment with no historical precedent.

Statutory Independence and the Maastricht Legal Framework

| Maastricht Pillar | Statutory Intent (1992) | Operational Reality (2010, 2026) |

|---|---|---|

| Article 130 (Independence) | Complete insulation from political pressure. No instructions taken. | Fiscal Dominance: The ECB is forced to keep rates manageable for high-debt states to prevent Eurozone fragmentation. |

| Article 123 (No Monetary Financing) | Strict ban on printing money to fund government deficits. | Secondary Market Loophole: Trillions in QE (PSPP, PEPP) funneled to governments via commercial banks. The distinction is legal, not economic. |

| Article 125 (No Bailout) | Market discipline; no mutualization of sovereign debt. | Implicit Guarantee: Instruments like OMT and TPI ensure the ECB intervene to cap spreads, mutualizing risk to save the currency. |

The "Stability Culture" exported by the Bundesbank assumed that rules would constrain behavior. History shows the opposite: behavior constrained the rules. The 2020-2026 period solidified a new legal doctrine where the preservation of the Eurozone takes precedence over the literal interpretation of the treaties. The ECB that without these interventions, the "transmission method" of monetary policy fails, meaning interest rate decisions in Frankfurt would not reach the real economy in Rome or Madrid. This argument, while economically defensible, represents a shift in the constitutional order. The ECB has transformed from a narrow guardian of price stability into a macroeconomic manager with the power to determine the solvency of nations. The "independent" central bank is the most political actor in Europe, deciding which spreads are "fundamental" and which are "unwarranted." The friction remains most acute in the definition of "Price Stability." The Maastricht Treaty did not define it numerically. The ECB's Governing Council defined it as ", close to, 2%," and later, following the 2021 strategy review, as a symmetric 2% target. This shift allowed for periods of overshoot, a flexibility that critics violates the strict stability mandate of the 1990s. By 2026, with inflation volatility returning as a structural feature of the global economy, the rigidity of the Maastricht framework looks increasingly like a relic of a bygone era, maintained in text abandoned in spirit. The "scar tissue" of the 1920s has been covered by the new scar tissue of the 2010s sovereign debt emergency. The ECB stands on a legal foundation that forbids it from doing exactly what it must do to survive.

Euro Introduction and the Transition from National Currencies (1999, 2002)

| Country | Legacy Currency | ISO Code | Rate (1 EUR =) |

|---|---|---|---|

| Germany | Deutsche Mark | DEM | 1. 95583 |

| France | French Franc | FRF | 6. 55957 |

| Italy | Italian Lira | ITL | 1936. 27 |

| Spain | Spanish Peseta | ESP | 166. 386 |

| Netherlands | Dutch Guilder | NLG | 2. 20371 |

| Belgium | Belgian Franc | BEF | 40. 3399 |

| Austria | Austrian Schilling | ATS | 13. 7603 |

| Portugal | Portuguese Escudo | PTE | 200. 482 |

| Finland | Finnish Markka | FIM | 5. 94573 |

| Ireland | Irish Pound | IEP | 0. 787564 |

| Luxembourg | Luxembourg Franc | LUF | 40. 3399 |

| Greece (Joined 2001) | Greek Drachma | GRD | 340. 750 |

The transition period from 1999 to 2001 operated under the legal principle of "no compulsion, no prohibition." Corporations and stock exchanges switched immediately; the Frankfurt DAX and Paris CAC 40 began quoting in Euros on January 4, 1999. Yet, for the average citizen, the Mark and Franc remained the tangible reality. Behind the scenes, the ECB and National Central Banks (NCBs) worked to integrate the plumbing of the financial system. The launch of TARGET (Trans-European Automated Real-time Gross Settlement Express Transfer System) connected the domestic payment systems, allowing a bank in Milan to settle a debt with a bank in Helsinki in real-time, eliminating the currency risk that had plagued cross-border trade for centuries. During this interim period, a twelfth member forced its way into the club. Greece, initially excluded for failing to meet the Maastricht convergence criteria, was admitted on January 1, 2001. Investigative analysis of this entry reveals a disturbing reliance on financial engineering rather than structural reform. In 2001, the Greek government, aided by Goldman Sachs, executed complex cross-currency swaps. These derivatives, specifically the "Aeolos" transaction, used fictitious historical exchange rates to mask approximately €2. 4 billion of sovereign debt, making it appear as a currency trade rather than a loan. This statistical sleight of hand allowed Athens to report debt-to-GDP ratios that technically, if deceptively, complied with Eurozone entry rules. The ECB and Eurostat later tightened reporting standards, the "original sin" of Greece's entry remained a dormant virus in the system, waiting to activate a decade later. The physical reality of the Euro arrived with the "Big Bang" cash changeover on January 1, 2002. This logistical operation dwarfs any other peacetime mobilization in European history. The Eurosystem produced an initial stock of 14. 9 billion banknotes and 52 billion coins. The total value of the notes alone exceeded €633 billion. If placed end-to-end, the banknotes would have reached the moon and back two and a half times; the coins weighed more than 24 Eiffel Towers. To prevent chaos on launch day, the ECB authorized "frontloading," a process where banks and retailers received cash shipments starting in September 2001. Armored convoys crisscrossed the continent, distributing the new currency to ATMs and vaults while strictly prohibiting its release to the public before Zero Hour. When the ATMs switched over at midnight on January 1, 2002, the psychological shock was immediate. The "Teuro" effect, a play on the German word *teuer* (expensive), became a dominant social narrative. While official Eurostat data showed aggregate inflation hovering near a benign 2%, public perception registered a massive spike in the cost of living. This gap stemmed from "menu costs" and opportunistic rounding. Restaurants, cafes, and service providers frequently converted prices at a 1: 1 or 2: 1 ratio for simplicity, ignoring the precise conversion rates. In Germany, a cup of coffee that cost 3 Marks frequently became 2 Euros, a mathematical increase of roughly 30%. The ECB struggled to counter this narrative, arguing that the price of durable goods like electronics had fallen, for the daily consumer, the Euro was synonymous with a loss of purchasing power. The death of the legacy currencies was swift. Within two months, the Deutsche Mark, a symbol of post-war stability and economic might, was withdrawn from circulation, stripped of its legal tender status on February 28, 2002. The French Franc, with a history stretching back to the 14th century, with equal speed. The NCBs collected and destroyed the old notes, shredding and briquetting billions of units of national history. This rapid demonetization prevented a prolonged period of dual circulation, forcing the Euro's acceptance. By the end of 2002, the transition was complete. The ECB controlled the money supply for over 300 million people. The National Central Banks, once the supreme monetary authorities of their respective, were reduced to operating arms of the Frankfurt-based Eurosystem. They retained their gold reserves and their staff, they lost the power to print money or set interest rates. The "One Size Fits All" monetary policy had begun, binding the industrial might of Germany to the agrarian and tourism-heavy economies of the South with a single interest rate, a structural rigidity that would face its existential test less than a decade later.

Eurozone Sovereign Debt Instability and Troika Intervention (2010, 2015)

The disintegration of the Eurozone's monetary illusion began not with a bank run, with a statistical correction. In late 2009, the newly elected Greek government revealed that the previous administration had underreported its budget deficit, revising the figure from a manageable 6% to a 12. 7% of GDP. This admission shattered the market's assumption that all Eurozone sovereign debt carried the same risk profile as German Bunds. By early 2010, the yield spreads between German debt and the "periphery", Greece, Ireland, Portugal, Spain, and Italy, widened violently. The method of monetary transmission, which the ECB relied upon to set interest rates across the bloc, fractured. A single interest rate set in Frankfurt no longer applied equally to a factory in Stuttgart and a construction firm in Seville.

The ECB's initial response was the Securities Markets Programme (SMP), launched in May 2010. This marked the central bank's significant deviation from its mandate of price stability into the murky waters of fiscal support. Under Jean-Claude Trichet, the ECB began purchasing the government bonds of distressed nations on the secondary market. By the time the program concluded in 2012, the ECB had accumulated approximately €218 billion in sovereign debt, primarily from Italy (€102. 8 billion), Spain (€44. 3 billion), and Greece (€33. 9 billion). While officially sterilized to prevent inflation, the SMP functioned as a backstop for governments that had lost market access. Critics, particularly at the Bundesbank, argued this violated Article 125 of the Lisbon Treaty, the "no bailout" clause. Yet, the alternative was the immediate insolvency of the Eurosystem.

As the emergency metastasized, the ECB's role shifted from liquidity provider to political enforcer. The most egregious example of this power occurred in Ireland. In November 2010, the Irish state guaranteed the liabilities of its collapsing banking sector, a decision that transferred private losses to the public balance sheet. On November 19, 2010, Jean-Claude Trichet sent a secret letter to Irish Finance Minister Brian Lenihan. The correspondence, kept hidden for years, contained an explicit threat: the ECB would cut off Emergency Liquidity Assistance (ELA) to Irish banks, destroying the nation's financial system, unless Ireland immediately applied for a bailout program. The letter stated, "it is only if we receive in writing a commitment from the Irish government... that we can authorise further provisions of ELA." Ireland capitulated, accepting an €85 billion rescue package and a harsh austerity regime dictated by the "Troika", the European Commission, the ECB, and the IMF.

The interplay between sovereign debt and banking stability created a "doom loop" that threatened to consume the currency union. European banks held vast quantities of their own governments' debt. As sovereign credit ratings collapsed, the value of this collateral fell, rendering the banks insolvent. The banks then required state bailouts, which further increased sovereign debt, causing yields to rise even higher. In March 2012, this pattern culminated in the restructuring of Greek debt, known as Private Sector Involvement (PSI). Private bondholders were forced to accept a 53. 5% nominal haircut, resulting in a real net present value loss of approximately 75%. This operation, the largest sovereign default in history, wiped out €107 billion in debt shattered the myth that Eurozone sovereign bonds were risk-free assets.

The turning point arrived not through policy, through rhetoric. By July 2012, Spanish 10-year bond yields had breached 7. 6%, a level considered unsustainable. Speculation about a breakup of the Eurozone mounted. On July 26, 2012, Mario Draghi, who had succeeded Trichet, delivered a speech in London that halted the panic. He declared, "Within our mandate, the ECB is ready to do whatever it takes to preserve the euro. And believe me, it be enough." The markets reacted instantly. Spanish 10-year yields fell 45 basis points, and Italian yields dropped 39 basis points. Draghi backed this verbal intervention with the announcement of Outright Monetary Transactions (OMT), a program allowing unlimited purchases of short-term sovereign bonds for countries that accepted strict conditionality. Although OMT was never activated, its existence acted as a "big bazooka," forcing speculators to retreat.

While OMT stabilized yields, the internal imbalances of the Eurosystem continued to widen, visible only in the obscure TARGET2 payment system. TARGET2 records cross-border flows between Eurozone central banks. As capital fled the periphery for the safety of the core, the liabilities of the central banks of Italy and Spain surged, while the claims of the German Bundesbank skyrocketed. By mid-2012, the Bundesbank's TARGET2 claims peaked at over €750 billion. This imbalance represented a silent, automatic bailout: the German central bank was lending money to the periphery to finance the purchase of German exports and the flight of capital back to Germany.

The final taboo was broken in Cyprus in 2013. The island nation's banking sector, bloated with Greek debt, collapsed. The Troika demanded a contribution from depositors to fund the rescue, a "bail-in" rather than a bailout. Initially, the plan proposed a levy on all deposits, including those under the €100, 000 insurance limit. Public outrage forced a revision, the final deal was severe. Uninsured depositors in the Bank of Cyprus faced a 47. 5% haircut, converted into equity, while Laiki Bank was wound down, wiping out uninsured deposits entirely. This event signaled a new regime: in the event of a widespread failure, depositor funds were no longer sacrosanct. The Cyprus bail-in established the template for the Bank Recovery and Resolution Directive (BRRD), codifying the rule that creditors and depositors must take losses before taxpayer money is used.

| Country | 10-Year Bond Yield Peak | Date of Peak | SMP Purchases (Est. € bn) | Troika Bailout Volume (€ bn) |

|---|---|---|---|---|

| Greece | > 35% (pre-PSI) | Feb 2012 | 33. 9 | 240 (Total Programs) |

| Ireland | 14. 2% | July 2011 | 13. 6 | 67. 5 |

| Portugal | 17. 4% | Jan 2012 | 21. 6 | 78. 0 |

| Spain | 7. 6% | July 2012 | 44. 3 | 41. 3 (Bank Rescue) |

| Italy | 7. 3% | Nov 2011 | 102. 8 | None |

By 2015, the immediate threat of a Eurozone breakup had receded, the cost was a fundamental transformation of the ECB. It had evolved from a technocratic institution modeled on the Bundesbank into a political power broker capable of dictating national fiscal policy, threatening banking systems with asphyxiation, and redistributing wealth across borders through its balance sheet. The austerity measures enforced by the Troika led to deep recessions in the periphery, with youth unemployment in Greece and Spain exceeding 50%. The stage was set for the phase of monetary experimentation: the battle against deflation and the launch of quantitative easing.

Asset Purchase Programmes and Balance Sheet Expansion (2015, 2019)

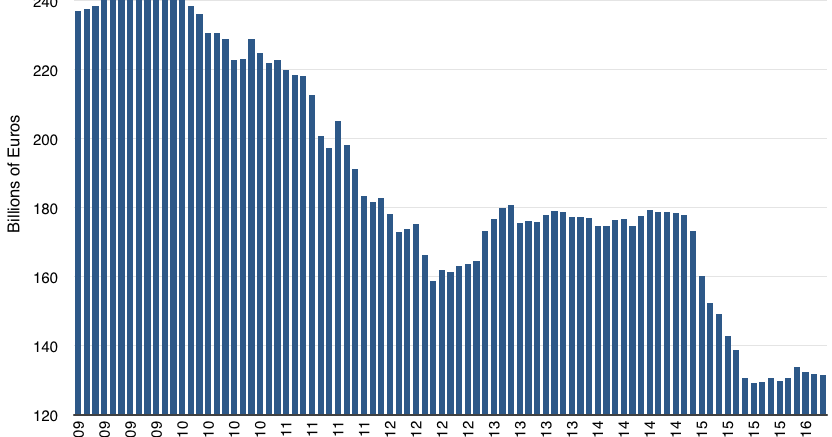

On March 9, 2015, the European Central Bank crossed a Rubicon that separated orthodox central banking from experimental monetary engineering. With the launch of the Public Sector Purchase Programme (PSPP), the ECB ceased to be a lender of last resort for banks and became the primary creditor of Eurozone governments. This was not a temporary liquidity; it was a structural transformation of the European bond market. Under the presidency of Mario Draghi, the Governing Council authorized the printing of €60 billion per month to purchase sovereign debt, a figure that would soon swell to €80 billion. The stated goal was to avert deflation and return inflation to the ", close to, 2%" target. The unstated reality was a massive suppression of yields that allowed highly indebted nations, specifically Italy, Spain, and France, to service debts that market forces would otherwise have rendered unsustainable.

The of this intervention dwarfs any prior monetary operation in the continent's history, exceeding the relative size of the Bank of England's balance sheet expansion during the Napoleonic Wars. By the end of 2019, the ECB's balance sheet had exploded from approximately €2 trillion to nearly €4. 7 trillion. This expansion was not driven by gold accumulation or productive assets, by the absorption of government paper and, controversially, corporate debt. The method broke the link between risk and yield. In 2015, German 10-year Bund yields turned negative for the time in history. Investors paid the German government for the privilege of lending it money, a financial anomaly that for years and destroyed the savings models of pension funds and insurance companies across the bloc.

The following table details the escalation of the Asset Purchase Programme (APP) and the simultaneous descent into negative interest rates, a dual-pronged strategy that defined the era.

| Year | Net Purchase Target (Monthly) | Deposit Facility Rate (DFR) | ECB Balance Sheet (Year End) | Key Policy Shift |

|---|---|---|---|---|

| 2015 | €60 Billion | -0. 20% to -0. 30% | €2. 7 Trillion | Launch of PSPP (Sovereign QE) |

| 2016 | €80 Billion | -0. 30% to -0. 40% | €3. 6 Trillion | Launch of CSPP (Corporate QE) |

| 2017 | €60 Billion | -0. 40% | €4. 4 Trillion | Reduction in monthly pace |

| 2018 | €30bn (Jan) / €15bn (Oct) | -0. 40% | €4. 6 Trillion | Net purchases halted in December |

| 2019 | €20 Billion (Restarted Nov) | -0. 50% | €4. 7 Trillion | Reversal of normalization policy |

In June 2016, the ECB radicalized its method by introducing the Corporate Sector Purchase Programme (CSPP). No longer content with sovereign bonds, the central bank began purchasing the debt of private corporations. This move shattered the pretense of market neutrality. The ECB subsidized the borrowing costs of multinational giants, including LVMH, Volkswagen, Shell, and Nestlé. By suppressing the yields on corporate bonds, the ECB allowed these incumbents to borrow at rates frequently lower than the inflation rate, while small and medium-sized enterprises (SMEs), which rely on bank loans rather than bond markets, saw little benefit. This "Cantillon Effect" redistributed wealth from the currency holders to the asset holders, fueling a stock market rally even as the real economy in the Eurozone periphery stagnated.

The selection criteria for CSPP holdings drew intense scrutiny. While the ECB claimed to follow a "market-neutral" benchmark, the portfolio heavily favored carbon-intensive industries and sectors dominated by legacy firms. Investigative analysis of the bond list revealed that the central bank was protecting "zombie firms", companies unable to cover debt servicing costs from operating profits, by ensuring a continuous flow of cheap credit. This prevented the creative destruction necessary for economic renewal, trapping capital in unproductive sectors. The ECB became a blind capital allocator, directing billions into the coffers of companies that had little need for public support, distorting price discovery method that had existed since the Amsterdam stock exchange of the 17th century.

Legal challenges to this monetary expansion mounted immediately. A group of German academics and politicians, led by Heinrich Weiss, filed suit, arguing that the PSPP violated Article 123 of the Treaty on the Functioning of the European Union (TFEU), which prohibits monetary financing of governments. The plaintiffs contended that the ECB was not conducting monetary policy economic policy, a domain reserved for member states. This legal battle culminated in the European Court of Justice (ECJ) ruling in Weiss (Case C-493/17) in December 2018. The ECJ upheld the legality of the program, accepting the ECB's argument that the purchases were proportional to the objective of price stability. Yet, the German Federal Constitutional Court (Bundesverfassungsgericht) remained skeptical, setting the stage for a constitutional emergency that would erupt in 2020. The tension between Karlsruhe and Frankfurt exposed the fragile legal architecture of the Euro: a currency without a state, managed by a bank that claimed unlimited power to preserve it.

Simultaneously, the ECB's Negative Interest Rate Policy (NIRP) eroded the profitability of the European banking sector. By charging banks a penalty rate (initially -0. 20%, eventually reaching -0. 50%) on excess reserves stored at the central bank, the ECB intended to force banks to lend to the real economy. The data suggests a different outcome. Banks, particularly in Germany and the Netherlands, faced compressed Net Interest Margins (NIM), which weakened their capital buffers. Instead of lending to risky startups, banks chose to pass the costs onto corporate depositors or increase fees, further dragging on economic activity. The policy acted as a tax on the banking system, extracting billions of euros annually from the financial sector to subsidize government deficits.

The "Capital Key", the rule dictating that ECB bond purchases must be proportional to a country's share of the ECB's capital (based on population and GDP), became a source of constant friction. To support the bond markets of weaker economies like Italy, the ECB frequently deviated from the strict capital key, buying a disproportionate amount of Italian debt relative to German debt. This created a system of fiscal transfers via the central bank's balance sheet, a method explicitly forbidden by the Maastricht Treaty. Critics argued that the ECB had become a "bad bank" for the Eurozone, warehousing the risk of insolvent states to prevent a sovereign debt emergency that market forces would otherwise have precipitated.

By late 2018, the Governing Council attempted to normalize policy. Net purchases were halted in December 2018, marking the end of the phase of quantitative easing. The balance sheet was meant to shrink as bonds matured. This resolve lasted less than a year. As manufacturing data from Germany and global trade tensions rose, the Eurozone economy began to stall. In September 2019, in one of his final acts as President, Mario Draghi reversed course. He announced the restart of net purchases at a rate of €20 billion per month and cut the deposit rate further to -0. 50%. This decision faced public dissent from the governors of the German, Dutch, Austrian, and French central banks, who argued that restarting the printing press was unnecessary and dangerous. The restart signaled that the ECB had entered a "debt trap": the system was so addicted to liquidity that even a modest attempt to withdraw it threatened collapse. The era of 2015, 2019 proved that once a central bank begins to monetize debt on a massive, the exit door is welded shut.

Pandemic Emergency Purchase Programme Execution (2020, 2022)

The Pandemic Emergency Purchase Programme (PEPP) stands as the single most aggressive monetary intervention in the history of the European Central Bank. It was not a liquidity provision. It was a suspension of the rulebook. In March 2020 the Eurozone bond market faced a terminal dislocation. Liquidity evaporated. Bid-ask spreads on Italian BTPs widened to levels not seen since 2012. The catalyst for this specific panic was not just the virus a communication failure on March 12 2020. President Christine Lagarde stated the ECB was "not here to close spreads." This single sentence shattered the ambiguity Mario Draghi had carefully constructed years earlier. Italian 10-year yields spiked by 60 basis points in hours. The risk of a sovereign debt spiral became immediate.

Frankfurt reversed course with extreme speed. On March 18 2020 the Governing Council announced the PEPP with an initial envelope of €750 billion. This figure later swelled to €1. 85 trillion through two subsequent expansions in June and December 2020. The defining feature of PEPP was not its size its flexibility. Previous programs like the Public Sector Purchase Programme (PSPP) bound the ECB to the "capital key." This rule dictated that bond purchases must strictly mirror a member state's shareholding in the ECB. Germany paid in the most capital so the ECB had to buy mostly German Bunds. PEPP explicitly discarded this constraint. The legal text allowed "fluctuations in the distribution of purchase flows over time, across asset classes and among jurisdictions."

This flexibility clause permitted the ECB to conduct a targeted bailout of the Italian and Spanish bond markets while pretending to run a general monetary policy operation. Data from the execution phase confirms this deviation. Between March 2020 and the end of net purchases in March 2022 the Eurosystem purchased Italian debt significantly above Italy's capital key. At peak stress moments in early 2020 the deviation exceeded 10 percentage points relative to the standard quota. The ECB absorbed the entire net issuance of Italian public debt during the pandemic emergency. This action transferred the insolvency risk of Rome directly onto the Eurosystem balance sheet.

| Jurisdiction | Capital Key Target (%) | Actual Purchase Share (%) | Deviation (approx. pp) |

|---|---|---|---|

| Germany | 26. 4% | 24. 9% | -1. 5% |

| France | 20. 4% | 19. 8% | -0. 6% |

| Italy | 17. 0% | 19. 2% | +2. 2% |

| Spain | 11. 9% | 12. 8% | +0. 9% |

| Others | 24. 3% | 23. 3% | -1. 0% |

The execution of PEPP faced a serious legal threat from Karlsruhe. On May 5 2020 the German Federal Constitutional Court issued its judgment in the Weiss case. The judges ruled that the ECB's previous bond-buying program (PSPP) absence a proper "proportionality assessment" and might be ultra vires (beyond its powers). While the ruling technically targeted the older program it cast a shadow over PEPP. The German court demanded the Bundesbank stop participating unless the ECB justified its actions. This created a standoff between German constitutional law and European Union supremacy. The ECB resolved this not by submitting to the German court by authorizing the Bundesbank to disclose internal documents that proved the "proportionality" of the measures. The emergency abated the legal fragility of the ECB's unlimited power remained exposed.

By late 2021 the macroeconomic problem shifted from deflation to inflation. The supply chain shocks and energy emergency forced a change in strategy. The Governing Council halted net asset purchases under PEPP in March 2022. The total cumulative net purchases reached approximately €1. 718 trillion. This portfolio did not. The ECB entered a reinvestment phase where it used the principal from maturing bonds to buy new ones. This phase maintained the stock of liquidity in the system even as interest rates began to rise. Crucially the ECB retained the right to use these reinvestments flexibly. If Italian yields spiked again the ECB could channel redemptions from German Bunds into Italian BTPs. This method served as a dormant defense line against market fragmentation.

The final of the PEPP infrastructure began in 2024. The Governing Council reduced the PEPP portfolio by €7. 5 billion per month starting in the second half of that year. By the end of 2024 full reinvestments ceased. As we examine the balance sheet in 2026 the legacy of PEPP is a massive block of low-yielding sovereign debt that drags on the ECB's profitability. The central bank operates with negative equity in real terms although accounting conventions mask the severity of the loss. The PEPP succeeded in preventing a Eurozone breakup in 2020. It did so by monetizing debt on a that made the ECB the dominant creditor of Eurozone governments. The distinction between monetary policy and fiscal support was not just blurred. It was erased.

Interest Rate Normalization and the 2022, 2024 Inflation Spike

| Date | Deposit Facility Rate (DFR) | Eurozone HICP Inflation | Eurosystem Balance Sheet (Approx.) |

|---|---|---|---|

| June 2022 | -0. 50% | 8. 6% | €8. 8 Trillion (Peak) |

| October 2022 | 1. 50% | 10. 6% (Peak) | €8. 7 Trillion |

| September 2023 | 4. 00% (Peak) | 4. 3% | €7. 0 Trillion |

| June 2024 | 3. 75% ( Cut) | 2. 5% | €6. 5 Trillion |

| March 2026 | 2. 00% | 1. 7% | €6. 3 Trillion |

### The Industrial Toll The aggressive normalization exposed the fragility of the Eurozone's export-led model. Germany, the bloc's engine, contracted by 0. 3% in 2023 and stagnated throughout 2024. Energy-intensive industries, chemicals, steel, and glass, faced a double shock: the loss of cheap Russian gas and the end of cheap capital. Production in these sectors remained nearly 15% pre-pandemic levels well into 2025. Critics argued that the ECB was fighting a supply-side war with demand-side weapons. Hiking rates could not reopen gas pipelines or fix semiconductor absence; it could only crush demand to match the constrained supply. By late 2024, this objective was achieved, at the cost of investment and growth. ### The Pivot and the Aftermath (2024, 2026) Recognizing the rapid cooling of the economy, the ECB cut rates for the time in June 2024, lowering the DFR to 3. 75%. A series of reductions followed, bringing the rate down to **2. 00%** by March 2026. Inflation, having been beaten down by the recessionary pressure, fell the 2% target, hovering around 1. 7% in early 2026. The 2022, 2024 episode remains a scar on the ECB's history. It revealed the limitations of forecasting models that rely heavily on linear extrapolations of the past. The central bank's hesitation in 2021 necessitated the brutality of 2023, creating a volatility trap that Europe is still working to escape. The "normalization" was anything normal; it was a forced march from one extreme to another, leaving a deindustrialized core in its wake.

Digital Euro Infrastructure and Central Bank Digital Currency Trials (2024, 2026)

By March 2026, the European Central Bank moved past theoretical white papers and entered the operational reality of the Digital Euro. Following the conclusion of the "Preparation Phase" on October 31, 2025, the Governing Council authorized the transition to the implementation stage, a decision that greenlit the construction of a parallel monetary rail for the Eurozone. This shift was not administrative; it involved the allocation of over €1. 1 billion in framework contracts to private vendors, cementing the technical architecture of the currency before the European Parliament had even finalized the legal regulation to govern it. The ECB's strategy became clear: build the machine, then wait for the legislative permission to switch it on.

The infrastructure procurement process, finalized in late 2025, revealed the extent to which the ECB has outsourced the nuts and bolts of sovereign money. While the central bank retains control over the ledger, the actual engineering relies heavily on a consortium of private entities. Giesecke+Devrient (G+D), a Munich-based security technology group with roots in printing banknotes since the 19th century, secured the largest slice of the budget, a contract with a ceiling of €662 million to develop the "offline" component of the Digital Euro. This specific award highlights the ECB's primary defensive argument against critics: the pledge that the Digital Euro function like physical cash, usable without an internet connection and offering a higher degree of privacy than commercial bank transfers.

The technical specifications for this offline capability, under active development, rely on "Secure Element" (SE) hardware in smartphones and smart cards. Unlike online transactions, which pass through the Eurosystem's settlement engine, offline payments settle peer-to-peer using near-field communication (NFC). The challenge facing G+D and the ECB throughout 2026 involves the "double-spending" problem. In a decentralized offline environment, the system must prevent a user from spending the same digital token twice without checking a central ledger. The solution uses the tamper-resistant hardware of the device itself to deduct the balance locally. This architecture creates a new battleground over hardware access; for the offline Euro to work on iPhones, Apple must grant the ECB's app access to the NFC chip, a privilege historically guarded behind the "Apple Pay" walled garden. The Digital Markets Act (DMA) provides the legal battering ram, yet the technical integration remains a source of friction.

Beyond the offline method, the ECB selected other vendors to manage the online ecosystem. Feedzai, a data science company, won the contract for risk and fraud management, while a consortium involving Almaviva and Fabrick took charge of the app and software development kit (SDK). The selection of European-domiciled firms for the majority of these contracts was a calculated political maneuver. During the earlier prototyping phase in 2022, the inclusion of Amazon caused a furor among EU lawmakers concerned about data sovereignty. By 2025, the ECB had corrected course, ensuring that the "strategic autonomy" of the payment rail was not compromised by reliance on American cloud giants, at least on paper.

The banking sector, represented by the European Banking Federation (EBF), intensified its lobbying efforts in 2025 and early 2026, focusing its fire on the "holding limit." Commercial banks fear that if citizens can hold unlimited funds directly with the central bank, they withdraw deposits from commercial accounts, depriving banks of the cheap funding used to underwrite loans. This process, known as disintermediation, threatens the fractional reserve model that has dominated European finance since the 19th century. To appease these fears, the ECB proposed a holding cap, widely discussed at €3, 000 per citizen. An October 2025 impact study released by the ECB argued that a €3, 000 limit would result in a manageable deposit outflow of approximately 2%, a figure the central bank deemed safe for financial stability.

To make this cap workable for daily use, the infrastructure includes a "waterfall" method. If a user receives a payment that pushes their balance over €3, 000, the excess immediately cascades into their linked commercial bank account. Conversely, if a user attempts to make a payment exceeding their Digital Euro balance, the system performs a "reverse waterfall," pulling the necessary funds instantly from their commercial bank. This design reduces the Digital Euro to a transactional pass-through vehicle for large sums, while allowing it to function as a store of value for smaller amounts. Critics this compromise creates a convoluted system that protects commercial bank profits at the expense of user simplicity, maintaining the "parasitic" relationship between public money and private credit institutions.

The legislative track remains the primary bottleneck. As of March 2026, the "Single Currency Package", the legal text proposed by the European Commission in June 2023, is still navigating the trilogue negotiations between the European Parliament, the Council, and the Commission. The "legal tender" status of the Digital Euro is the most contentious point. The ECB insists that for the currency to be a true public good, merchants must be legally obliged to accept it. Retailers push back against mandatory acceptance, citing the costs of upgrading point-of-sale terminals. Meanwhile, privacy advocates in the Parliament demand legally binding guarantees that the ECB cannot technically monitor offline transactions, refusing to accept mere policy assurances.

The trials scheduled for 2026 focus on integrating these systems. The ECB is currently running "end-to-end" testing, simulating the flow of funds from a commercial bank account, through the waterfall method, into the Digital Euro wallet, and to a merchant settlement. These tests are not public pilots internal stress tests designed to break the system before the public touches it. The complexity of synchronizing the central bank's ledger with the legacy IT systems of thousands of Eurozone banks is immense. A single failure in the waterfall method could leave a user unable to pay or, worse, cause funds to in transit between the commercial and central bank ledgers.

Historians of monetary policy view the Digital Euro not as a novelty, as a return to the pre-fractional reserve era of the Bank of Amsterdam. The Amsterdamsche Wisselbank (1609, 1820) operated on a near-100% reserve basis; the guilders in its ledger represented actual metal in the vault, not credit created by lending. Similarly, the Digital Euro represents a liability of the central bank, backed 100% by the ECB's balance sheet, bypassing the money-creation multiplier of commercial banks. This structural reality terrifies the commercial banking sector more than the technology itself. If the holding limit were ever raised or removed, the Digital Euro would resurrect the "Chicago Plan" of the 1930s, ending the private sector's privilege of money creation. The €3, 000 cap is the only dam holding back this structural revolution.

| Component | Primary Contractor | Function | Strategic Implication |

|---|---|---|---|

| Offline Solution | Giesecke+Devrient (G+D) | Secure Element-based P2P payments | Enables "cash-like" privacy and resilience without internet. |

| Risk & Fraud | Feedzai | Transaction monitoring | Real-time surveillance of online transaction patterns. |

| Alias Lookup | Sapient & Tremend | Linking IBAN/Phone to ID | Connects digital identity to the payment rail. |

| App & SDK | Almaviva & Fabrick | User Interface | Standardizes the wallet experience across the Eurozone. |

The timeline for the public launch has slipped. While earlier projections hoped for a 2026 rollout, the reality of the legislative gridlock and the technical density of the offline solution has pushed the target to 2029. The years 2024 through 2026 be recorded as the period where the "theoretical" Digital Euro died, and the "industrial" Digital Euro, a complex, compromised, and heavily contracted beast, was born. The ECB is no longer asking if it should problem the currency, is instead spending billions to ensure that when the political green light flickers on, the engine already be idling.

Grossmarkthalle Headquarters Site and Construction Cost Overruns

The physical seat of the European Central Bank in Frankfurt am Main represents a collision between high-finance ambition and one of the darkest chapters in German history. Located in the Ostend district, the headquarters integrates the Grossmarkthalle, a wholesale market hall built between 1926 and 1928, with a modern twin-tower skyscraper. The site itself demands rigorous examination, not as an architectural feat as a crime scene. Between 1941 and 1945, the Gestapo used the cellar of this specific building as a collection point for the deportation of approximately 10, 000 Jews from Frankfurt to concentration camps. The ECB did not simply buy a plot of land; it acquired a heavy historical load that required the integration of a memorial directly into the facility's perimeter.

Architect Martin Elsaesser designed the original Grossmarkthalle, which stood as a monument to the "New Frankfurt" modernist movement. Its barrel-vaulted concrete shells, spanning 220 meters, were an engineering marvel of the 1920s. When the ECB purchased the site in 2002, the challenge was to preserve this protected landmark while constructing a secure, high-tech command center for the Eurozone. The Vienna-based architectural firm Coop Himmelb(l)au won the design competition with a deconstructivist proposal that pierced the historic hall with a twisted, glass-and-steel double tower rising 185 meters. The design intended to symbolize transparency and efficiency. The execution, yet, demonstrated the opposite.

The financial planning for the headquarters stands as a testament to the inability of central planners to forecast their own capital expenditures. In 2005, the ECB estimated the total investment cost at €850 million. This figure was supposed to cover the land purchase, the restoration of the Grossmarkthalle, and the construction of the new towers. By the time the building opened in 2015, the final price tag had swollen to approximately €1. 3 billion. This 53% overrun occurred during a period when the ECB demanded fiscal austerity from member states like Greece and Italy, creating a clear optical dissonance that critics frequently.

Several specific factors drove this budget explosion. The primary driver was the condition of the 1928 Grossmarkthalle. Initial surveys failed to detect the severity of the structural weaknesses in the concrete shell and the contamination in the ground. Restoring the thin, reinforced concrete vaults required complex, custom-engineered solutions that standard construction schedules. The "vegetable cathedral," as it was once known, proved far more resistant to modernization than the bankers had anticipated. Also, the price of steel and glass spiked globally between 2010 and 2012, driven by demand in Asian markets, forcing the ECB to pay premiums to secure materials.

The project faced a catastrophic setback in June 2013 when the primary construction contractor, Alpine Bau, filed for insolvency. Alpine Bau was the second-largest construction company in Austria, and its collapse was the largest bankruptcy in the country since 1945. The insolvency halted work on the site, threw the supply chain into chaos, and forced the ECB to scramble for new contractors to finish the job. This disruption alone added months of delays and tens of millions of euros to the final bill, as the bank lost the use of a fixed-price contract and had to negotiate with smaller firms in a seller's market.

| Year | Project Stage | Estimated/Actual Cost | Key Event |

|---|---|---|---|

| 2005 | Initial Planning | €850 Million | Original budget approval based on 2005 prices. |

| 2010 | Construction Start | €1. 0 Billion (Revised) | Groundbreaking; adjustments for material inflation. |

| 2012 | Topping Out | €1. 2 Billion (Revised) | Admission of €350m overrun due to "unforeseen" structural work. |

| 2013 | emergency Point | Unknown | Alpine Bau declares bankruptcy; site work paralyzed. |

| 2015 | Completion | €1. 3 Billion (Final) | Official opening amidst anti-austerity protests (Blockupy). |

The integration of the Holocaust memorial, designed by architects KatzKaiser, serves as the only element of the project that proceeded with appropriate. The memorial preserves the ramp and the cellar used by the Gestapo, keeping them accessible to the public and separate from the high-security zones of the bank. It creates a physical void in the, a concrete scar that interrupts the parkland surrounding the glass towers. This proximity forces a daily confrontation between the technocratic present and the genocidal past. The ECB deserves credit for not erasing this history, yet the juxtaposition remains jarring: the of European monetary union humming directly above the station where thousands were sent to their deaths.

By 2026, the headquarters has settled into its role as a fixed asset on the Eurosystem's balance sheet, the financial irony. In February 2026, the ECB reported a loss of €1. 3 billion for the fiscal year 2025, a figure eerily identical to the construction cost of its building. These operational losses, stemming from high interest payments on excess liquidity, mean the bank burned through the equivalent of its entire headquarters' value in a single year of negative income. The "Skytower" stands not just as a symbol of the Euro, as a monument to the colossal of expenditures that define modern central banking, both in concrete and in capital.

The operational costs of the facility continue to draw scrutiny. The high-tech atrium, designed to function as a "vertical city," requires massive energy inputs for climate control, challenging the building's green credentials. While the design includes geothermal heating and rainwater harvesting, the sheer volume of glass creates a greenhouse effect that demands aggressive cooling during Frankfurt's increasingly hot summers. The maintenance of the restored Grossmarkthalle concrete also presents an ongoing liability; the material, nearly a century old, requires constant monitoring to prevent spalling and carbonation, ensuring that the preservation costs did not end with the opening ceremony in 2015.

The Grossmarkthalle project reveals the limitations of the ECB's technocratic competence. The institution that claims to model the future inflation of the entire Eurozone failed to predict the inflation of its own housing project by a margin of 50%. The reliance on a single massive contractor, Alpine Bau, mirrored the widespread risk the bank is supposed to police in the financial sector. When that "too big to fail" contractor failed, the ECB was left holding the bill, a microcosm of the sovereign debt bailouts that defined the era of the building's construction.

Litigation Regarding Ultra Vires Acts and Proportionality

The existential threat to the European Central Bank has frequently emerged not from bond markets or inflation prints, from the austere courtrooms of Karlsruhe, Germany. While the Governing Council in Frankfurt operates under the assumption of federal supremacy, the German Federal Constitutional Court (Bundesverfassungsgericht or BVerfG) has spent two decades constructing a legal around the concept of ultra vires, acts beyond the powers conferred by treaties. This legal warfare reached a fever pitch between 2020 and 2026, challenging the very foundation of the Eurosystem: the idea that the ECB is the sole master of its own mandate. The conflict rests on a single, razor-thin distinction between "monetary policy," which is the ECB's exclusive domain, and "economic policy," which remains the prerogative of member states.

The prelude to this constitutional collision began with the Gauweiler litigation in 2012, challenging the Outright Monetary Transactions (OMT) program. Peter Gauweiler, a Bavarian politician, argued that Mario Draghi's "whatever it takes" pledge amounted to illicit state financing. The BVerfG referred the case to the Court of Justice of the European Union (CJEU), marking the time the German court had ever solicited a preliminary ruling from Luxembourg. The CJEU ruled in 2015 that OMT was legal, provided the ECB did not hold bonds to maturity and respected certain purchase limits. The German judges accepted this interpretation with gritted teeth, issuing a warning that future programs would face stricter scrutiny regarding their specific design and volume.

That warning materialized with explosive force on May 5, 2020, in the Weiss judgment (2 BvR 859/15). In a ruling that shook the legal foundations of the European Union, the BVerfG declared that the ECB's Public Sector Purchase Program (PSPP) constituted an ultra vires act. More shockingly, the German judges declared the CJEU's prior approval of the program to be "objectively arbitrary" and "methodologically untenable." This was a judicial declaration of war: a national court asserting that the highest European court had failed to do its job, thereby rendering its judgment non-binding in Germany. The core of the dispute was not whether the ECB could buy bonds, whether it had proven that the benefits of doing so outweighed the collateral damage to savers, pension funds, and real estate prices.

The Weiss ruling introduced a strict requirement for a "proportionality assessment" (Verhältnismäßigkeitsprüfung). The court argued that the ECB had focused so myopically on its inflation target that it ignored the "economic policy effects" of its actions. By flooding the market with liquidity, the central bank was conducting fiscal policy, redistributing wealth and keeping insolvent zombies alive, without the democratic legitimacy of a parliament. The BVerfG gave the ECB three months to produce a document proving that the PSPP was proportional. Failure to comply would have forced the Bundesbank, the ECB's largest shareholder, to cease participation in the program and sell its bond holdings, a move that would have likely triggered a sovereign debt emergency in Italy and Spain.

| Case Name | Year | Target Program | Core Legal Argument | Outcome |

|---|---|---|---|---|

| Gauweiler | 2015 | OMT | Illicit monetary financing of states. | CJEU approved; BVerfG accepted with conditions. |

| Weiss | 2020 | PSPP | Violation of proportionality; Ultra vires act. | BVerfG declared CJEU ruling invalid; demanded proof. |

| Gunther | 2022 | PEPP | Pandemic emergency powers exceeded mandate. | Dismissed, established stricter review limits. |

| Climate Action | 2025 | Green Framework | Mandate creep into industrial policy. | Pending; draft EU resolution challenges "green" focus. |

The standoff was resolved through a diplomatic fudge. The ECB, refusing to submit directly to the jurisdiction of a German court, released "non-public" documents to the German government and parliament, which then satisfied the court's requirements. Yet the precedent was set: the ECB's independence is not absolute, and its actions are subject to review for proportionality. This legal sword of Damocles hangs over the Transmission Protection Instrument (TPI), announced in July 2022. Unlike previous programs, the TPI allows for chance unlimited bond purchases to counter "unwarranted" market. Legal scholars that the TPI absence the clear quantitative limits that saved the OMT in the Gauweiler case. The definition of "unwarranted" implies that the ECB possesses superior knowledge of a country's fundamental fiscal health compared to the market, a claim that invites aggressive litigation.

By 2024 and 2025, the legal terrain shifted toward the ECB's expanding "green" mandate. In January 2026, the ECB announced it had fully climate and nature-related risks into its supervisory and monetary policy frameworks. This move, while praised by environmental groups, triggered immediate legal pushback. A draft EU resolution in late 2025 highlighted the friction, reminding the ECB that its primary objective is price stability, not environmental protection. Critics that by tilting its collateral framework to favor "green" assets, the ECB is engaging in active industrial policy, picking winners and losers based on carbon intensity rather than credit risk. This opens a new front for ultra vires challenges, as opponents that climate policy is the exclusive preserve of elected parliaments, not unelected technocrats.

The concept of "mandate creep" has thus moved from academic debate to active litigation. The Weiss judgment established that the ECB must provide a "comprehensible" account of how it balances its objectives. If the central bank suppresses yields for a high-debt nation under the TPI, or penalizes a fossil-fuel company under its green framework, it must prove these actions are necessary for price stability and not a of secondary political goals. The absence of such proof renders the acts void in Germany. This creates a "bicephalous" legal reality where an ECB action might be legal in Paris illegal in Berlin, a structural fracture that remains the single greatest long-term risk to the euro's survival.

The data on bond purchases reveals the of this legal risk. During the height of the PSPP, the ECB frequently method the self-imposed issuer limit of 33%, a constraint designed to prevent the central bank from becoming a blocking minority in debt restructurings. The Weiss litigation forced the ECB to acknowledge these limits explicitly. Yet, the Pandemic Emergency Purchase Program (PEPP) and subsequent tools removed of these safeguards, citing emergency conditions. As the "emergency" fades, the legal justification for these unbounded powers evaporates, leaving the ECB to a new wave of constitutional complaints that the bank has permanently crossed the Rubicon from monetary authority to economic government.

2025, 2026 Green Monetary Policy and Collateral Framework Adjustments

| Asset Class (Non-Financial Corp) | Base Haircut (Pre-2026) | Climate Factor Adjustment | Final Collateral Value Impact |

|---|---|---|---|

| Renewable Energy Utility (Green Bond) | 12. 0% | +0. 0% (Neutral) | No Change |

| Diversified Manufacturer (Transition Plan) | 12. 0% | +2. 5% | Marginal Reduction |

| Fossil Fuel Major (No Transition Plan) | 12. 0% | +6. 6% to +10. 0% | Serious Liquidity Drag |

The enforcement of these rules depends entirely on data availability, leveraging the European Union's Corporate Sustainability Reporting Directive (CSRD). The ECB made disclosure a hard eligibility requirement: assets issued by companies that fail to report emissions data under CSRD standards are barred from the collateral pool. This requirement closes the loophole where opacity acted as a shield. In 2024, a absence of data frequently resulted in a neutral score; in 2026, the absence of data results in ineligibility. This shift compels even private, non-listed entities to adopt rigorous carbon accounting if they wish their debt to remain bankable in the Eurosystem. Isabel Schnabel, the Executive Board member most associated with this green pivot, argued in her May 2025 Stanford speech that this method is necessary for price stability, not just environmental protection. She contended that "fossilflation", price volatility driven by dependence on carbon-intensive energy, poses a greater long-term threat to the ECB's inflation mandate than the short-term costs of transition. Yet, this stance invites serious political friction. Critics that penalizing energy companies during periods of supply constraint exacerbates inflation, creating a feedback loop where the central bank's green policies directly conflict with its primary target of 2% inflation. Looking beyond carbon, the ECB's 2024-2025 "Climate and Nature Plan" set the stage for the frontier: biodiversity. By early 2026, the bank began integrating "nature-related risks" into its analytical models, acknowledging that ecosystem collapse presents a financial stability risk distinct from climate change. While the current collateral framework focuses on carbon transition risks, the inclusion of nature degradation metrics, such as water usage and deforestation footprints, is the logical step in the ECB's risk assessment evolution. The bank is signaling that the destruction of natural capital soon carry a liquidity cost, just as carbon emissions do today. The transition from the Bank of Amsterdam's metal-backed ledger to the ECB's climate-adjusted collateral framework represents a total inversion of monetary philosophy. Where the Wisselbank sought trust through the physical immutability of gold, the ECB seeks stability through the managed adaptation of the economy. The 2026 framework asserts that a currency cannot be stable if the biosphere it operates within is collapsing. By pricing environmental risk into the heart of the repo market, the ECB has weaponized its balance sheet to force a transition that politics alone failed to accelerate.